The loan provider's rights over the protected residential or commercial property take top priority over the debtor's other creditors, which suggests that if the debtor ends up being bankrupt or insolvent, the other creditors will only be paid back the debts owed to them from a sale of the protected property if the home loan loan provider is paid back in complete first.

Couple of people have adequate cost savings or liquid funds to enable them to purchase residential or commercial property outright - how to reverse mortgages work if your house burns. In nations where the demand for own a home is greatest, strong domestic markets for home loans have developed. Home mortgages can either be funded through the banking sector (that is, through short-term deposits) or through the capital markets through a procedure called "securitization", which transforms pools of mortgages into fungible bonds that can be sold to investors in little denominations.

Total Payment (3 Fixed Rate Of Interest & 2 Loan Term) = Loan Principal + Costs (Taxes & costs) + Total interest to be paid. The final cost will be precisely the very same: * when the interest rate is 2. 5% and the term is 30 years than click here when the rates of interest is 5% and the term is 15 years * when the interest rate is 5% and the term is thirty years than when the rate of interest is 10% and the term is 15 years According to Anglo-American residential or commercial property law, a mortgage takes place when an owner (normally of a cost easy interest in realty) promises his or her interest (right to the residential or commercial property) as security or security for a loan.

As with other kinds of loans, mortgages have an rate of interest and are arranged to amortize over a set amount of time, usually thirty years. All types of genuine property can be, and typically are, protected with a mortgage and bear a rate of interest that is supposed to reflect the lender's threat.

Although the terms and accurate types will vary from nation to nation, the standard parts tend to be comparable: Residential or commercial property: the physical residence being financed. The precise kind of ownership will differ from country to country and might limit the types of financing that are possible. Home mortgage: the security interest of the lender in the home, which may involve limitations on the use or disposal of the property.

Some Known Incorrect Statements About How Many Mortgages Are Backed By The Us Government

Borrower: the person loaning who either has or is creating an ownership interest in the residential or commercial property. Loan provider: any lending institution, however generally a bank or other monetary institution. (In some nations, especially the United States, Lenders might likewise be investors who own an interest in the home mortgage through a mortgage-backed security.

The payments from the customer are thereafter gathered by a loan servicer.) Principal: the original size of the loan, which may or might not consist of certain other costs; as any principal is repaid, the principal will go down in size. Interest: a financial charge for use of the lender's money.

Completion: legal conclusion of the home mortgage deed, and thus the start of the home loan. Redemption: final payment of the amount exceptional, which may be a "natural redemption" at the end of the scheduled term or a swelling amount redemption, typically when the debtor decides to offer the property. A closed home loan account is said to be "redeemed".

Federal governments typically regulate lots of elements of home mortgage lending, either directly (through legal requirements, for example) or indirectly (through guideline of the participants or the monetary markets, such as the banking market), and typically through state intervention (direct lending by the federal government, direct loaning by state-owned banks, or sponsorship of numerous entities).

Home loan are typically structured as long-lasting loans, the routine payments for which resemble an annuity and computed according to the time worth of cash formulae. The most standard plan would require a repaired monthly payment over a duration of 10 to thirty years, depending upon regional conditions.

Examine This Report about In What Instances Is There A Million Dollar Deduction Oon Reverse Mortgages

In practice, numerous variations are possible and common worldwide and within each nation. Lenders supply funds against residential or commercial property to make interest earnings, and usually borrow these funds themselves http://jasperqcnk880.yousher.com/how-reverse-mortgages-work-in-maryland-things-to-know-before-you-buy (for instance, by taking deposits or issuing bonds). The price at which the lending institutions obtain money, therefore, impacts the expense of loaning.

Home mortgage loaning will likewise consider the (viewed) riskiness of the mortgage loan, that is, the likelihood that the funds will be paid back (usually considered a function of the creditworthiness of the customer); that if they are not paid back, the loan provider will have the ability to foreclose on the real estate properties; and Browse around this site the monetary, interest rate threat and dead time that might be involved in particular scenarios.

An appraisal might be ordered. The underwriting process may take a couple of days to a couple of weeks. Sometimes the underwriting procedure takes so long that the provided monetary declarations need to be resubmitted so they are present (how do reverse mortgages work in utah). It is suggested to maintain the exact same work and not to use or open new credit throughout the underwriting process.

There are many kinds of home mortgages used worldwide, however numerous factors broadly specify the attributes of the home mortgage. All of these may be subject to local guideline and legal requirements. Interest: Interest might be repaired for the life of the loan or variable, and change at specific pre-defined periods; the interest rate can also, obviously, be higher or lower.

Some mortgage might have no amortization, or require complete repayment of any remaining balance at a certain date, or perhaps unfavorable amortization. Payment amount and frequency: The amount paid per period and the frequency of payments; sometimes, the quantity paid per duration might alter or the customer might have the alternative to increase or decrease the amount paid.

8 Simple Techniques For How Do Reverse Mortgages Work When You Die

The two basic types of amortized loans are the fixed rate mortgage (FRM) and adjustable-rate mortgage (ARM) (also called a floating rate or variable rate mortgage). In some nations, such as the United States, repaired rate home loans are the norm, but drifting rate home mortgages are fairly typical. Combinations of fixed and drifting rate home loans are likewise common, whereby a home loan will have a fixed rate for some duration, for example the very first 5 years, and vary after the end of that period.

When it comes to an annuity payment scheme, the regular payment stays the exact same amount throughout the loan. When it comes to linear payback, the routine payment will gradually reduce. In a variable-rate mortgage, the interest rate is normally fixed for a duration of time, after which it will regularly (for example, each year or monthly) change up or down to some market index.

Given that the risk is moved to the customer, the initial rates of interest might be, for instance, 0. 5% to 2% lower than the average 30-year fixed rate; the size of the rate differential will be connected to debt market conditions, including the yield curve. The charge to the customer relies on the credit danger in addition to the interest rate danger.

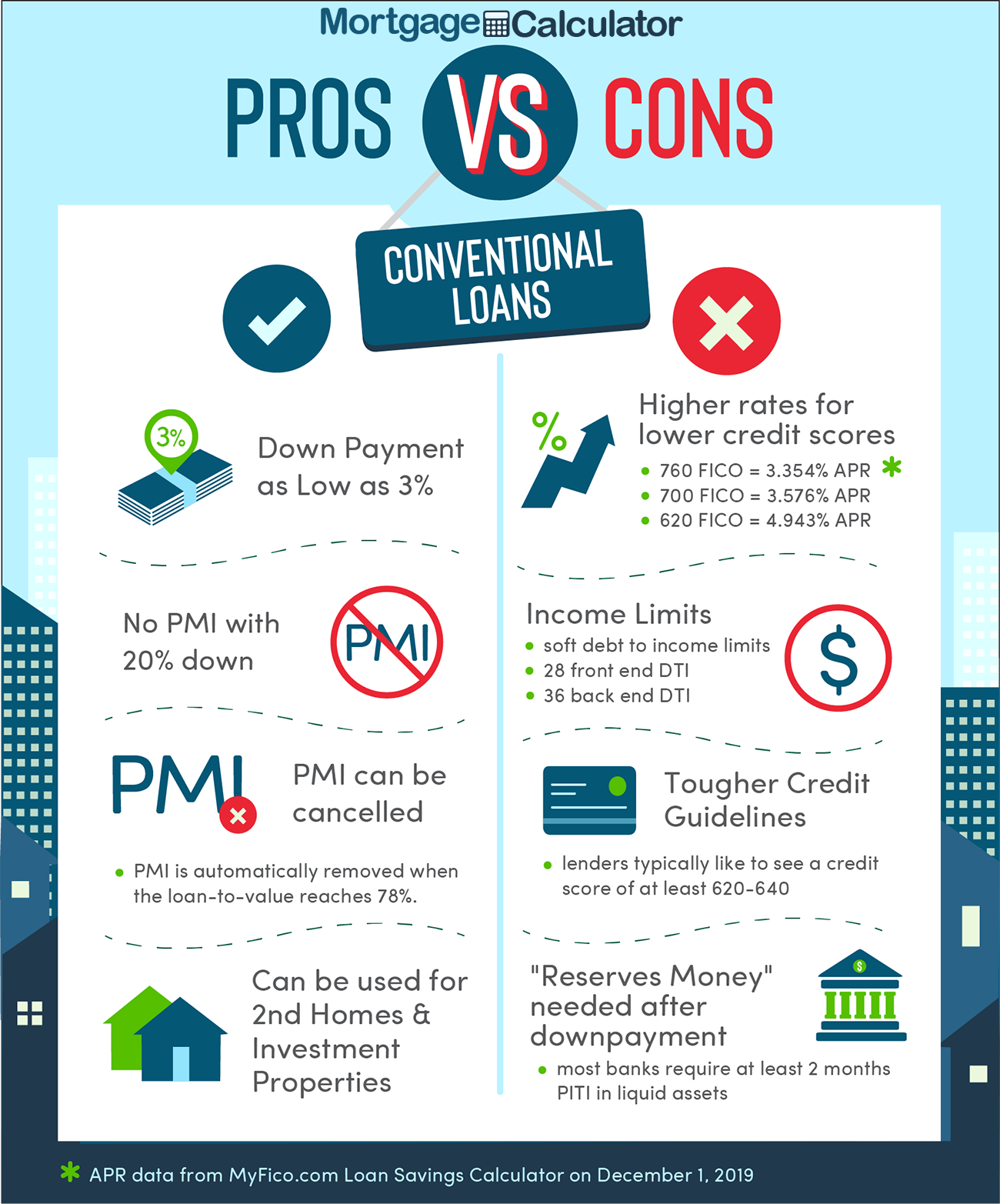

Jumbo home loans and subprime lending are not supported by federal government assurances and deal with higher interest rates. Other developments described listed below can impact the rates too. Upon making a home loan for the purchase of a residential or commercial property, lenders typically need that the customer make a deposit; that is, contribute a portion of the cost of the home.