Moderate income is specified as the higher of 115% of the U.S median family income or 115% of the state-wide and state non-metro median household incomes or 115/80ths of the area low-income limit. These USDA loan limitations are based upon both the regional market conditions and the family size. The moderate earnings warranty loan limitation is the exact same in any offered area for households of 1 to 4 individuals & is set to another level for homes of 5 to 8 individuals.

Location 1 to 4 Individual Limit 5 to 8 Person Limit Fort Smith, AR-OK MSA $78,200 $103,200 Northwest Arctic District, AK $157,850 $208,350 Oakland-Fremont, CA HUD Metro $145,700 $192,300 San Francisco, CA HUD Metro $202,250 $266,950 The floor worths on the above limits are $78,200 and $103,200 respectively. Houses with more than 8 individuals in them can add 8% for each extra member.

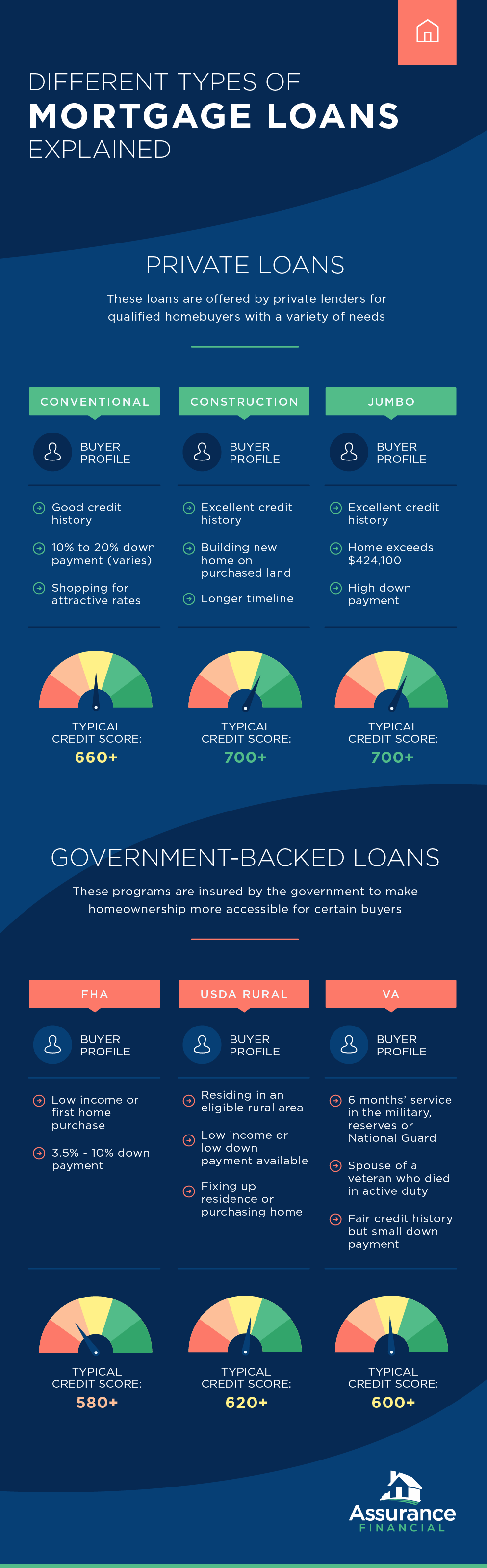

Loans can be utilized for routine, manufactured or modular homes which are no more than 2,000 square feet in size. The effective loan limitation starts at $125,500 in inexpensive areas and goes as high as $508,920 in pricey parts of California. You can see loan quantity limits in your area here.

This kind of loan is considered to be riskier because the payment can change substantially. In exchange for the danger connected with an ARM, the property owner is rewarded with a rates of interest lower than that of a thirty years fixed rate. When the homeowner gets a one year adjustable rate mortgage, what they have is a 30 year loan in which the rates change every year on the anniversary of the loan.

Lots of house owners with incredibly big home loans can get the one year adjustable rate mortgages and refinance them each year. The low rate lets them buy a more costly home, and they pay a lower home loan payment so long as interest rates do not rise. The loan is thought about to be rather risky since the payment can change from year to year in substantial quantities.

The 10/1 ARM has an initial interest rate that is fixed for the very first 10 years of the loan. After the ten years is up, the rate then adjusts each year for the rest of the loan. The loan has a life of thirty years, so the homeowner will experience the initial stability of a thirty years mortgage at a cost that is lower than a set rate mortgage of the exact same term.

The Facts About How Much Does A Having A Cosigner Help On Mortgages Uncovered

An adjustable rate home loan that has the very same rates of interest for part of the home mortgage and a different rate for the remainder of the home loan is called a 2-step home mortgage. The rate of interest modifications or changes in accordance to the rates of the current market. The borrower, on the other hand, may have the alternative of making the option between a variable interest rate or a fixed rates of interest at the change date.

Many debtors who take the two-step mortgage have plans of refinancing or vacating the house before the period ends. The 5/5 and the 5/1 adjustable rate home loans are amongst the other kinds of ARMs in which the month-to-month payment and the interest rate does not change for 5 years.

That's every year for the 5/1 ARM and every 5 years for the 5/5. These specific ARMs are best if the house owner intends on living in the home for a duration greater than 5 years and can accept the modifications later on. The 5/25 mortgage is also called a "30 due in 5" home loan and is where the regular monthly payment and rate of interest do not alter for 5 years.

This suggests the payment will not alter for the rest of the loan. This is a great loan if the homeowner can endure a single modification of payment throughout the loan duration. Mortgages where the monthly payment and rates of interest remains the very same for 3 years are called 3/3 and 3/1 ARMs.

That is 3 years for the 3/3 ARM and each year for the 3/1 ARM. This is the type of home loan that benefits those considering an adjustable rate at the three-year mark. Balloon home mortgages last for a much shorter term and work a lot like a fixed-rate home mortgage.

The factor why the payments are lower is due to the fact that it is primarily interest that is being paid monthly. Balloon home loans are great for accountable borrowers with the intents of selling the house prior to the due date of the balloon payment. Nevertheless, homeowners can run into big problem if they can not manage the balloon payment, particularly if they are required to refinance the balloon payment through the lender of the original loan.

All about How Would A Fall In Real Estate Prices Affect The Value Of Previously Issued Mortgages?

United States 10-year Treasury rates have actually just recently fallen to all-time record lows due to the spread of coronavirus driving a threat off sentiment, with other monetary rates falling in tandem. House owners who purchase or refinance at today's low rates may gain from current rate volatility. Are you paying excessive for your home mortgage? Check your re-finance choices with a relied on Mountain View lending institution.

Are you getting prepared to dive into your very first home purchase? If so, it might assist to discover the terminology when going over mortgages - what are cpm payments with regards to fixed mortgages Hop over to this website rates. As soon as you have these terms down, you'll be able to knowledgeably review the types of home loan choices available. Don't stress, you'll move into your new home in no time! Traditional fixed rate loans are a winner due to the fact that of their consistency the regular monthly payments won't change over the life of your loan.

They're available in 10, 15, 20, 30, and 40-year terms but 15 and 30 are the most typical. Interest-only home loans offer you the choice, throughout the first five or ten years, to pay only the interest part of your month-to-month payment instead of the complete payment. You aren't needed do this.

Afterward, the remainder of the home mortgage is paid off in complete like a conventional home loan. There are several ARMs. The Helpful resources basic concept is that their interest rate changes over time throughout the life of the loan. The rate modifications show modifications in the economy and the cost of obtaining money.

These are mortgages ensured by the Federal Real Estate Administration. They come with integrated home loan insurance coverage to secure against the possibility of not being able to pay back the loan. The needed down payments are smaller with these loans. These loans make it simpler for veterans of the U.S. militaries, and sometimes their partners, to purchase homes.

The combination takes place when you put a deposit of less than 20% and take two loans of any type in combination to prevent paying Private Home loan Insurance. On a balloon mortgage, you pay interest just for a certain time period 5 years for example and after that the overall principal quantity is due after this preliminary period.

4 Easy Facts About Which Of These Events Would Most Likely Lead To A Rise In Interest Rates For Home Mortgages Explained

Presently, the limitation has to do with $700,000. This means that the borrower would not get the most affordable rates of interest readily available on smaller rent your timeshare sized loans.